Award-winning PDF software

990-pf estimated tax payments Form: What You Should Know

The Form W-8BEN-E is used for: — To prove your foreign status. — To prove the existence of a U.S. relationship (e.g., for tax or other tax benefits). — To prove your eligibility for a U.S. withholding exemption. — To document an inheritance by a foreign beneficiary. — To document a marriage or other relationship entered into with a foreign legal entity (e.g., a partnership, S corporation or LLC) or individuals (e.g., a trust). — To provide a tax form to a foreign person who is not obligated to provide a U.S. tax return as a U.S. citizen or resident. — To provide a tax form to a U.S. person who is not required to have a U.S. tax return filed on a U.S. basis (or who may have not filed one because of a U.S. exit from the treaty country). To complete the W-8BEN-E, you must attach the following documents to each of the following four pages and to its cover sheet: Part I — A U.S. tax return, with both the income tax and the withholding exemptions. Form 941-X, U.S. Individual Income Tax Return (Individual) This form may be filed electronically using TurboT ax or you may complete the form using Form 1040EZ or 1040 (or a combination). A completed form is attached during the return preparation phase of the business or organization. Part II — A U.S. Tax return, with both the income tax and the withholding exemptions. Form 1040EZ, U.S. Individual Income Tax Return (Individual) This form may be filed electronically using TurboT ax or you may complete the form using Form 1040, 1040A or 1040EZ (or a combination). A completed form is attached during the return preparation phase of the business or organization. Part III — The certification from the U.S. consular officer. TFR Form W-8BEN — W-8BEN-E -W-8BEN (10/2021) (2016, 2017, 2018, 2019) Form W-8BEN-E (Rev. October 2021) (2017, 2018, 2019, 2020, 2021) (Rev.

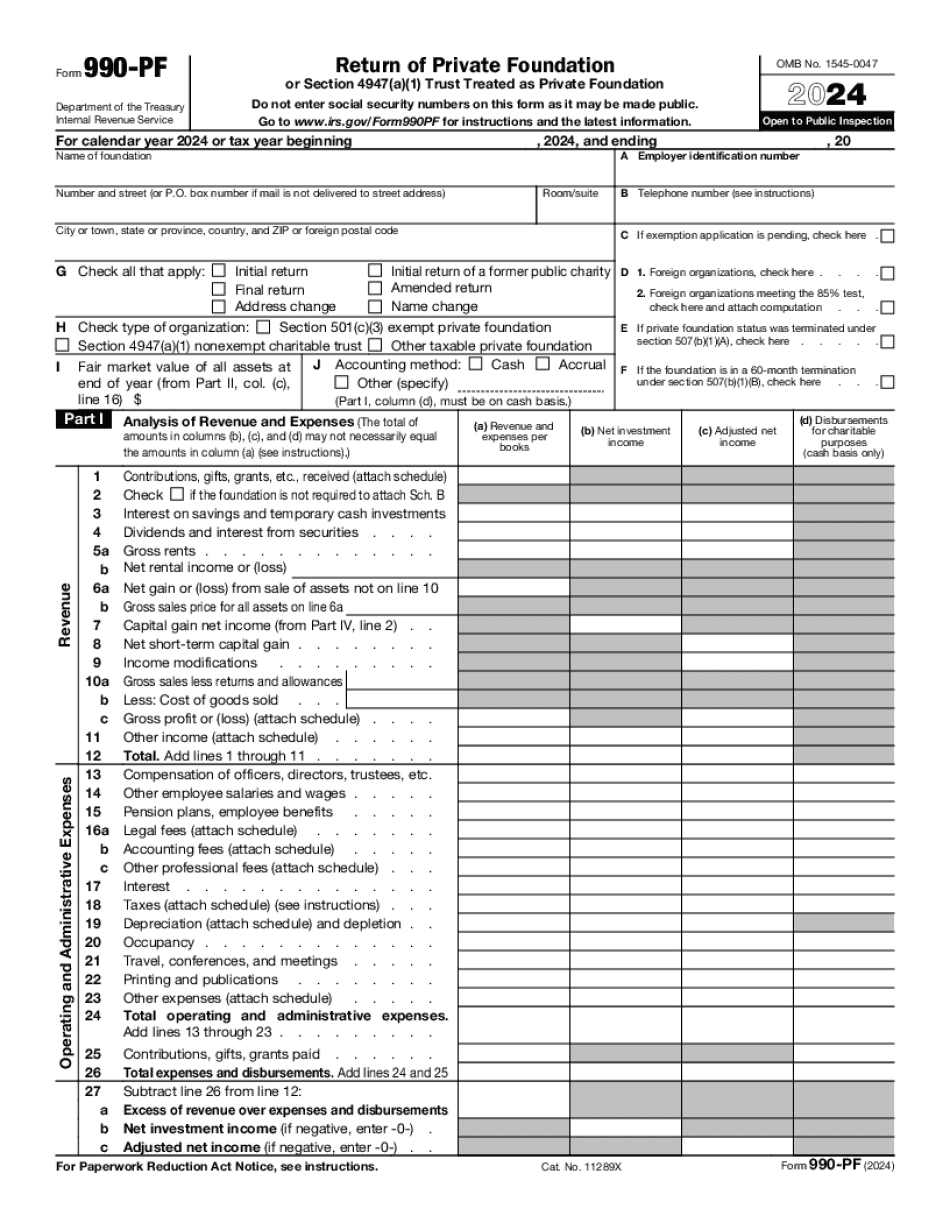

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 990-PF, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 990-PF online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 990-PF by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 990-PF from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.