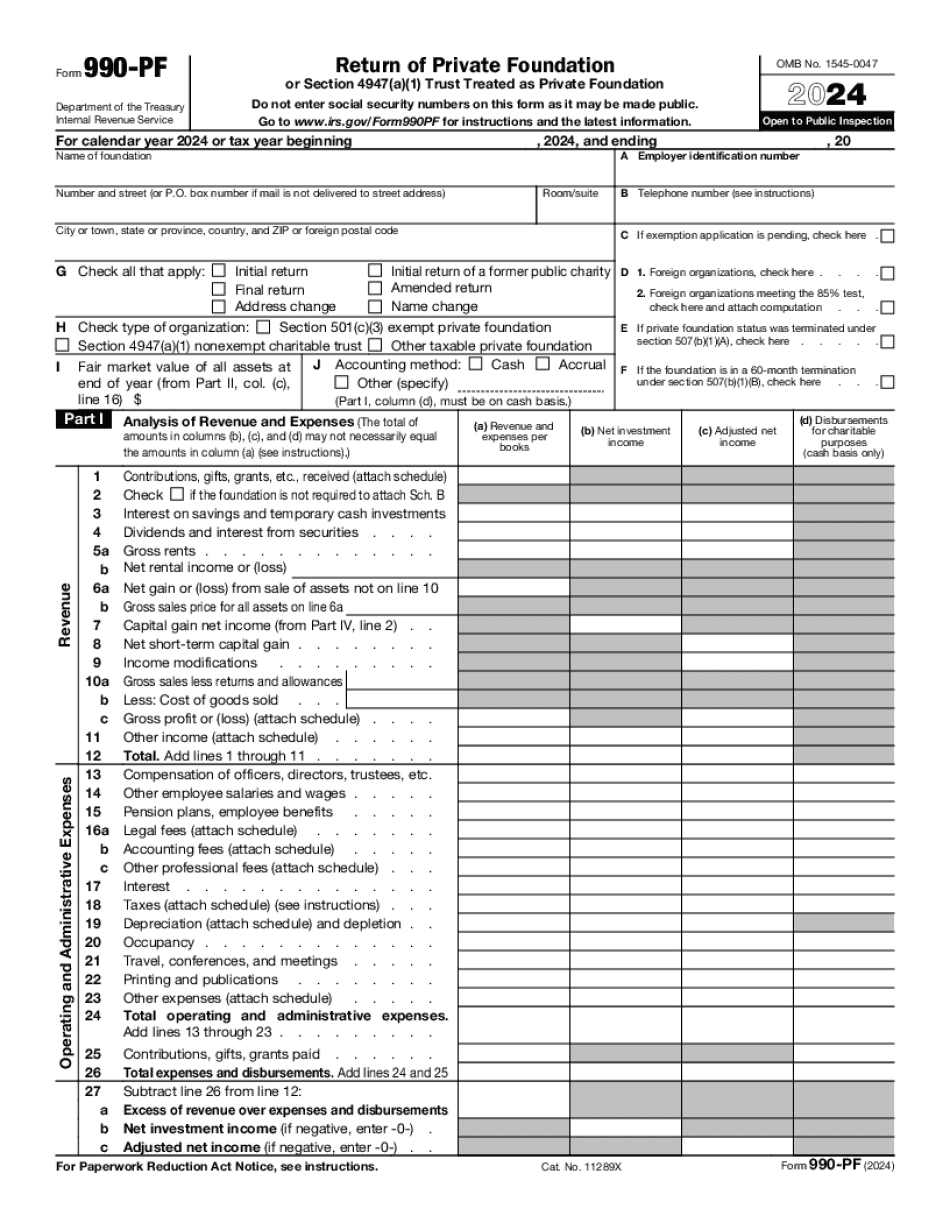

Private foundations are a unique class of 501(c)(3) organization. In fact, they have their own exclusive version of IRS Form 990, called the Form 990-PF. Hi, I'm Greg McCray, CEO of Foundation Group, and in this video, we're going to examine just what makes IRS Form 990-PF so different from its counterparts. Well, like a lot of the other Form 990s that we've talked about, the 990-PF requires details about expenses and revenue by category. However, because this is for private foundations only, these disclosures are really more concerning things that are in line with private foundations, which is different than what you would typically see with public charities. So, from a financial standpoint, what you see is a lot of focus on things like investments, endowments, earnings, and capital gains. It's a little bit different than the typical donation or program service revenue type disclosures that you see with a public charity. Now, people still donate to private foundations, so it's not like that information isn't there. But what you do see is a disproportionate share of attention paid to things revolving around endowments or investments. You also see something called a calculation of an excise tax on capital gains or investment earnings. That's also something that small excise tax is something that you do not see public charities pay. Something else that is unique about private foundations and the 990-PF is disclosure revolving around disqualified persons. Now, this qualified person is someone the IRS considers to be an insider, such as a board member, a key employee, maybe a large contributor, or a family member of the same. These people can usually easily be paid as an employee of a public charity, assuming that the right arm's length transactions are in place to get that person hired. In a private...

Award-winning PDF software

990-PF Form: What You Should Know

When you receive a CDP, you must complete it before leaving the IRS facility. If you are asked by the IRS to attend a hearing, you do not have the option of leaving the hearing until you have made a claim for relief. The only exceptions to this are when you receive an administrative summons from the IRS (or you are a witness who has been called as a witness, and you request a leave of absence) and you complete and attach form 8857 on the day you receive the summons. The IRS may also require you to attend a hearing while you are in the Federal Prison. This may occur if you are incarcerated with respect to a criminal case. In that case, you will be able to make a final decision about your claim for relief, but the IRS will not require you to appear in the hearing. You can't file a CDP or leave after your hearing. Your hearing occurs, as the hearing is not a formal order and order has no force until you have heard your claim for relief. The only exception to the hearing rule is if you receive an administrative summons from the IRS. In that case, you can receive the summons in the mail and complete Form 12153, and then mail it to your hearing officer as soon as you receive it. When you receive an administrative summons from the IRS, you must complete and attach Form 8857 with the other documentation and submit the forms and supporting documentation with a check or money order made out to the United States Treasury. If you are not able to comply with all required procedures to file your CDP or leave, or if you have concerns about the fairness of the hearing process, you should ask for a private hearing before an impartial third party. When your claim is settled or denied You can pay a portion of the tax balance you owe by using Form 1040X (or any other form). This is called the “payment in lieu of the filing of a claim” and is similar to the “tax offset” that you file on line 11 of your 1040. The payment must be made by direct deposit to the appropriate IRS account. You must enter the amount of the payment (a claim for refund, tax offset, refundable credit, tax arbitrage or a penalty) on line 11 of your 1040 as an offset to your tax liability. If you don't have enough withholding credits to make the full payment, follow the directions on the back of form 1040X for the amount you need to deposit directly to your bank account.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 990-PF, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 990-PF online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 990-PF by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 990-PF from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Form 990-PF